The Trillion-Dollar Trio Goes Public: What Advisors Need to Know About SpaceX, Anthropic, and OpenAI

- Jul 1

- 10 min read

For three years, clients have asked the same question: “How do I get into SpaceX or OpenAI before the IPO?” That question just changed tense. SpaceX has completed its roadshow and begins trading, Anthropic filed confidentially on June 1, and OpenAI followed on June 8 — a once-in-a-generation cluster of mega-listings, now all compressed into a single window. This piece covers what is confirmed, what is merely reported, how and when clients can actually invest, the unusual lock-up and float mechanics, and the index-inclusion question that will quietly determine billions in passive flows.

Why this matters now

Investors currently own none of these companies through their core portfolios — and yet within weeks, some of them will own one through QQQ whether they choose to or not. The gap between private-market innovation and public-market access, which has widened for a decade, is closing abruptly and at unprecedented valuations. The advisor’s job is to separate the genuine businesses (which are substantial) from the entry prices (which embed a lot of heroically optimistic assumptions), and to explain the unusual market structure these deals carry.

Where each company stands

At a glance:

| Status | Reported valuation | Latest revenue | Profitability | Listing window | Index path |

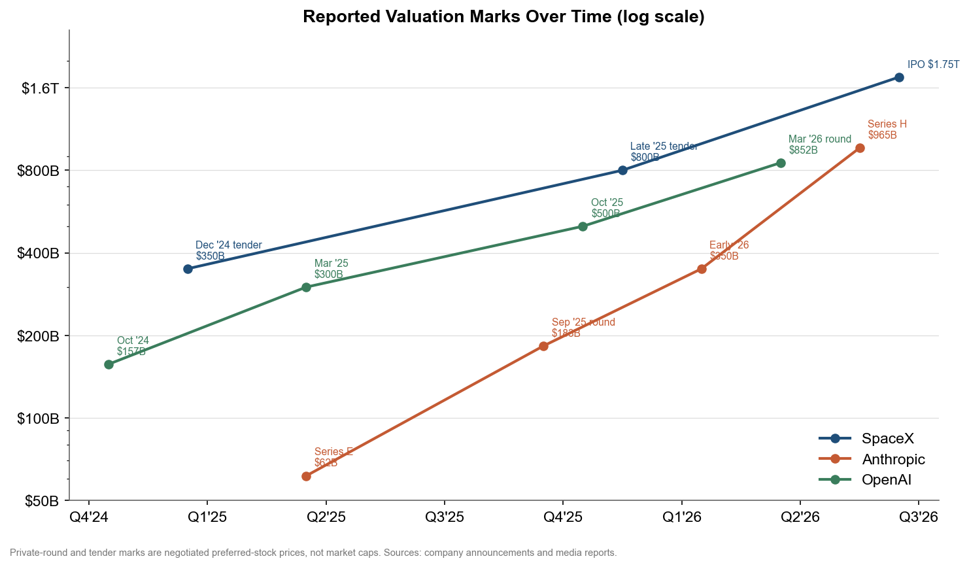

SpaceX | Trading on Nasdaq (SPCX) since June 12 | $1.75 trillion | $18.7B FY2025 (+33%) | GAAP net loss ~$5B (xAI integration); ~$6.6B adj. EBITDA | Now | NDX entry Jul 7 (confirmed); S&P 500 excluded |

Anthropic | Confidential S‑1 filed June 1 | $965 billion (Series H) | $47B run-rate (May 2026) | Operating profit reported Q2 2026 (unaudited) | October 2026 (reported) | TBD; S&P path shorter if profitability holds |

OpenAI | Confidential S‑1 filed June 8 | $852 billion (post-money) | ~$25B annualized (est.) | Projected 2026 loss ~$14B (burn est. up to ~$27B) | Delayed to 2027 (reported) | S&P 500 excluded for years; NDX-eligible |

Figures for Anthropic and OpenAI are company-announced or media-reported, not audited public disclosures.

SpaceX (Nasdaq: SPCX — trading now). SpaceX filed its S-1 on May 20, targeting roughly a $1.75 trillion valuation and a raise of up to $75 billion — the largest IPO in history, surpassing Saudi Aramco’s 2019 record. The offer priced at a fixed $135 per share, with first trading on Nasdaq on June 12. The fundamentals: 2025 revenue of $18.7 billion, up 33% from $14.1 billion in 2024, with roughly $6.6 billion of adjusted EBITDA but a GAAP net loss driven by stock compensation, satellite depreciation, and AI capex. The roughly $5 billion 2025 loss is largely attributable to the integration of xAI, which SpaceX acquired in February 2026. Starlink is the engine: connectivity revenue reached $3.26 billion in Q1 2026 — about 69% of the total — with 10.3 million subscribers, roughly double a year earlier. The honest framing for clients: at $1.75 trillion, SpaceX trades at roughly 94 times 2025 revenue while posting GAAP losses — a multiple that assumes flawless execution, but not that far off from what we saw in peak NVDA valuations.

Anthropic (confidential S-1 filed June 1). Anthropic submitted its draft registration statement on June 1, less than a week after closing a $65 billion Series H that pushed its valuation to $965 billion. The company has reported a revenue run-rate of $47 billion as of May 2026, up from roughly $10 billion in annual revenue the prior year, driven by enterprise adoption and coding products. By many metrics, Anthropic is likely the fastest-growing company in financial history. Goldman Sachs, JPMorgan, and Morgan Stanley are reportedly under consideration for lead roles, and multiple reports point to an October 2026 listing target — though confidential filings carry no committed timeline. (Disclosure note: run-rate and growth figures are company-announced, not yet audited public disclosures.)

OpenAI (confidential S-1 filed June 8). OpenAI confirmed its confidential filing on June 8, but on June 25 it postponed its listing to 2027 — reportedly after SpaceX’s volatile debut made its advisors more cautious, and after CEO Sam Altman declined to cut the company’s roughly $1 trillion valuation target to get a deal done sooner. Its most recent round — $122 billion at an $852 billion post-money valuation — included reported participation of $50 billion from Amazon, $30 billion from NVIDIA, and $30 billion from SoftBank, with the company citing more than 900 million weekly ChatGPT users and enterprise at over 40% of revenue. The tension is cash: revenue surpassed a $20 billion annualized pace by end-2025, but the company does not expect profitability until around 2030, with projected 2026 losses around $14 billion (other estimates of 2026 burn run as high as approximately $27 billion). OpenAI has raised more than $180 billion to date and is still burning cash to secure compute and build infrastructure.

Since the debut: a volatile first two weeks

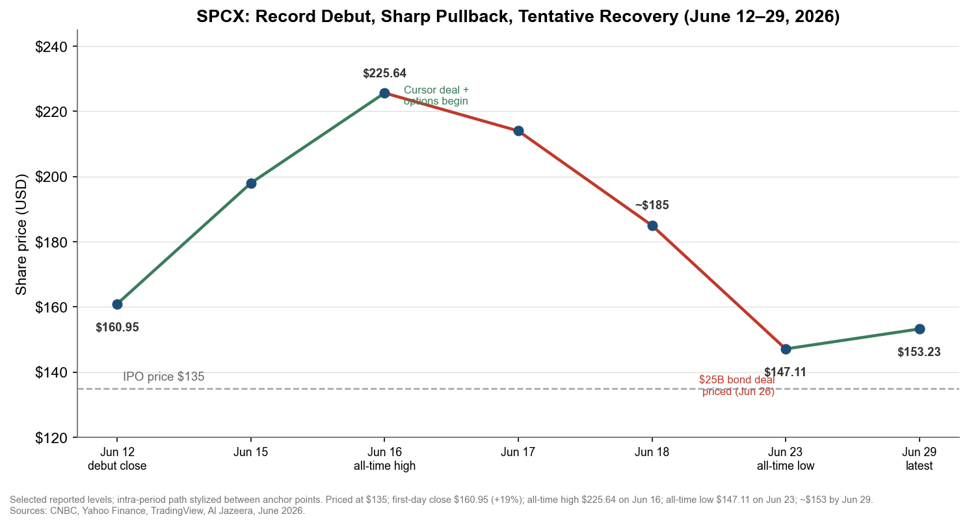

SpaceX’s first two weeks as a public company became a live demonstration of the scarcity dynamics described below. After pricing at $135, the stock opened around $150 and closed its first session at $160.95, a 19% gain. It then ran to an all-time high of $225.64 on June 16 — roughly 67% above the IPO price — before reversing just as sharply: three consecutive down days, including a double-digit intraday drop on June 22, pulled it back to an all-time low of $147.11 on June 23. At the trough the company had shed on the order of $600 billion of market value in three trading days; it has since stabilized, trading near $153 by June 29. Even after the round trip, the stock sits modestly above where it priced — a reminder that, with so little stock trading, price is set at the margin and swings wildly in both directions.

Two corporate actions amplified the move. On June 16, SpaceX announced a $60 billion all-stock acquisition of Cursor, an AI coding startup — roughly 3.4% dilution, and an unambiguous signal that the company intends to compete head-on with Anthropic and OpenAI in developer tools, building on its February 2026 absorption of xAI. Then, about ten days after the IPO, SpaceX launched its first-ever investment-grade bond offering, which priced at $25 billion of senior notes — upsized from a $20 billion target after drawing roughly $89 billion of orders, across five tranches maturing 2031 to 2056 — to refinance a bridge loan and fund its AI ambitions; all three major rating agencies assigned investment-grade ratings, and the filing disclosed roughly $100.8 billion of cash as of June 19. Layering debt on top of a fresh equity raise, together with the approaching lock-up calendar, is what cooled the initial euphoria.

How and when clients can invest

SpaceX: the window for IPO allocation has closed; from June 12 forward, this is an exchange-traded stock. Notably, SpaceX directed a percentage in the low 20s of the offering to retail buyers — below the roughly 30% originally planned, but still among the largest retail tranches ever for a U.S. IPO of this size (typical retail allocation is 5–10%). Allocated retail investors face anti-flipping restrictions imposed by brokerages.

Anthropic and OpenAI: there is nothing to buy yet, and that point deserves emphasis. A confidential filing does not put shares on sale; stock only becomes buyable after the IPO is priced and listed, which may be months away — and clients should be especially wary of anything claiming to offer pre-IPO shares, including crypto-platform derivative products that synthetically track estimated valuations. Legitimate pre-IPO access exists only through accredited-investor secondary platforms (Forge Global, Hiive, EquityZen) and certain pre-IPO interval funds — typically at wide bid offer spreads, with stale marks and no liquidity guarantee. For most clients, the realistic options are: (1) wait for the listing, (2) accept indirect exposure through public shareholders and partners (Microsoft, Amazon, Alphabet, NVIDIA), or (3) accept index-driven exposure as inclusion occurs.

The lock-up structure: tranching, not a cliff

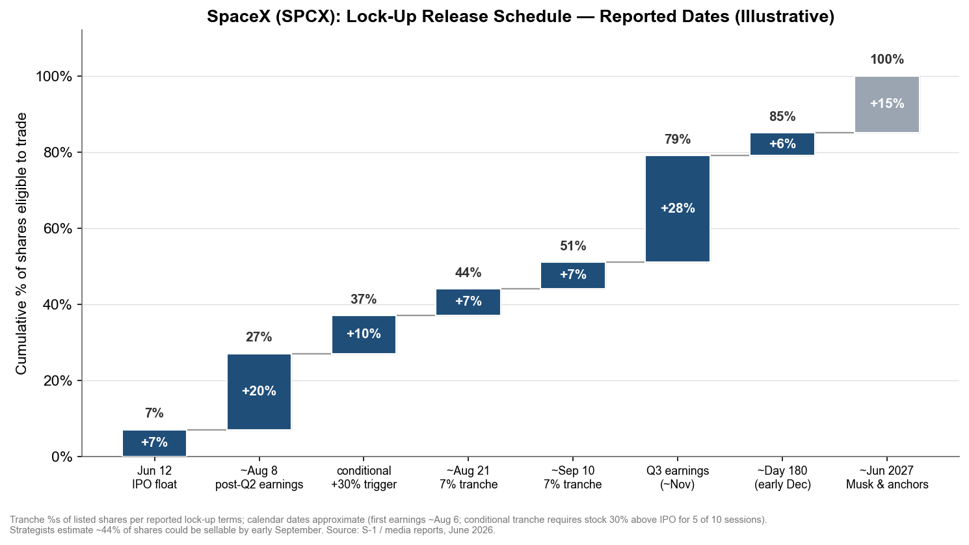

This is the most unusual feature of the SpaceX deal and the one advisors most need to understand, because it governs when supply hits the market. Instead of a single 90–180 day lock-up, SpaceX designed a rolling release: two days after its first earnings report, insiders can sell up to 20% of holdings; another 10% unlocks early if the stock holds 30% above the IPO price for five of ten consecutive trading days; 7% tranches free up at intervals through the first 135 days; a further 28% follows Q3 earnings; and the remainder releases at the standard 180-day point. Musk and select major backers committed to a full 366-day lock-up.

Why structure it this way? The design appears to be a response to Nasdaq’s new rules: the exchange relaxed its float requirements but gives low-float companies a reduced index weighting until more shares trade — so SpaceX has an incentive to ramp its float quickly after listing. The float math is striking: only around 7% of listed shares will be freely tradable at launch, and some estimates put true initial float nearer 3–4% of total shares. Expect Anthropic and OpenAI to study this template closely.

The takeaway here is that early price action will reflect scarcity, not consensus valuation. Each unlock tranche is a scheduled supply event, and the staggered structure means insiders can begin selling far earlier than the typical 180 days — into demand that index funds are mechanically required to provide. That dynamic is no longer hypothetical: with SpaceX’s first earnings report expected around August 6, strategists now estimate insiders could be free to sell as much as 44% of shares by early September — expanding the tradable float by roughly 900%.

Index inclusion: the quiet main event

Index treatment is where these IPOs diverge most sharply, and where clients holding “passive” funds need to understand what they actually own.

S&P 500 — excluded for now. S&P Global declined to change its criteria, including the requirement that a company be profitable — shutting SpaceX out of quick inclusion given its $4.94 billion 2025 net loss. S&P 500 entry requires positive trailing GAAP earnings plus float and seasoning standards, so SPY/VOO/IVV holders get no exposure for at least a year, likely longer. The same hurdle awaits OpenAI (deeply unprofitable) for years; Anthropic’s path could be shorter if reported profitability materializes.

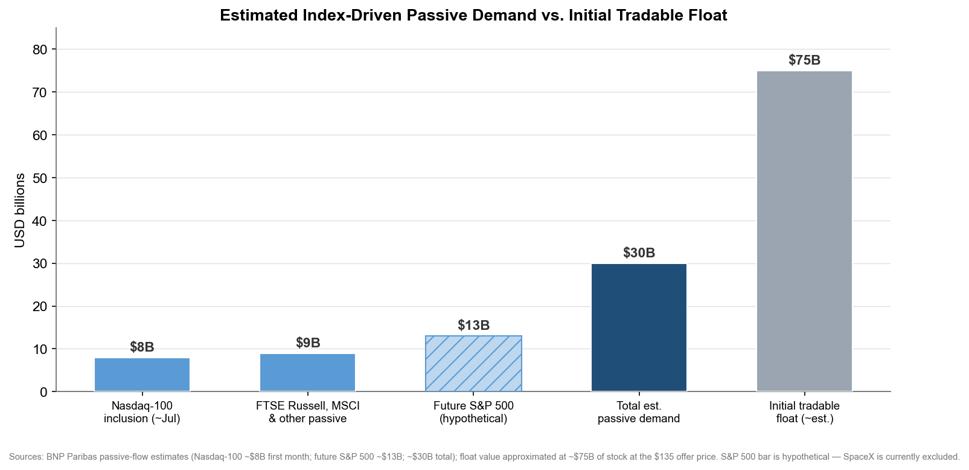

Nasdaq-100 — fast-tracked. Under Nasdaq’s new “fast entry” rule effective May 1, companies whose market caps rank within the top 40 of the index become eligible for inclusion within 15 trading days of IPO, versus roughly three months previously — and fast entries don’t require dropping an existing member. Nasdaq also scrapped its 10% free-float requirement for large caps, instead applying a multiplier-based weighting; FTSE Russell shortened its window to five trading days, and MSCI confirmed fast-track provisions for large IPOs. Nasdaq has confirmed SpaceX will join the Nasdaq-100 before the open on July 7 — 15 trading days after its IPO, the fastest inclusion in the index’s history — with index-tracking funds buying after the close on July 6; options on the stock began trading June 16. At current valuations, SpaceX, OpenAI, and Anthropic would all qualify for fast entry.

Index | Profitability requirement | Float requirement | Fast-entry window |

S&P 500 | Positive trailing GAAP earnings required | Float and seasoning standards apply | None — no fast entry |

Nasdaq-100 | None | 10% free-float rule scrapped for large caps; multiplier-based weighting | Top-40 market caps: within 15 trading days of IPO |

FTSE Russell | None | Standard float rules | Window shortened to 5 trading days |

MSCI | None | Standard float rules | Fast-track provisions confirmed for large IPOs |

The flow consequence. BNP Paribas estimates Nasdaq-100 inclusion alone will generate roughly $8 billion of passive buying in the first month, with a future S&P 500 inclusion worth another ~$13 billion, and total passive demand around $30 billion; index-forecast firm Intropic estimates passive investors will hold approximately 30% of SpaceX’s free float within 15 trading days. A tiny float meeting tens of billions in mechanical demand is a recipe for volatility in both directions — and clients in QQQ are buyers at whatever price prevails, while S&P 500 investors sit out entirely. That’s a genuine divergence between “index funds” that clients think of as interchangeable.

Valuation context advisors can use

It’s important to differentiate the three as very different investments. SpaceX at ~$1.75T is a profitable-infrastructure story (Starlink) bundled with two expensive options (Starship which if it comes fully online is a payload monopoly into outer space and may be the true intrinsic value to bolster current optimistic valuations; the xAI stack which is second-rate at this point) at ~94x revenue. Anthropic at $965B is the fastest enterprise revenue ramp ever reported, priced near 20x a run-rate that is itself five months old. OpenAI at ~$852B is the largest consumer AI franchise, priced against the deepest cash burn with plans to monetize through advertising. Public registration will expose actual revenue and margins for the first time — a direct confrontation between valuations and disclosed numbers — and the supply pressure is already reshaping the calendar — rather than risk a discounted listing, OpenAI pushed its IPO to 2027, leaving SpaceX and Anthropic as the near-term tests of public appetite. Private-round marks are negotiated prices for preferred stock with protections; they are not market caps, and clients should not anchor based on them.

For the two pure AI Labs, the other looming question that may affect valuations and future revenue and earnings growth is regulation, namely the government’s decision to limit or deny the ability of both companies to release their latest state-of-the-art models.

Practical guidance for client conversations

Position sizing matters more than timing. If a client insists on participation, treat it as a speculative satellite position (low single-digit percent), acknowledge the lock-up calendar as a known supply schedule, and avoid chasing the scarcity-driven first few weeks. For diversified exposure, the indirect route remains underrated: Microsoft, Amazon, Alphabet, and NVIDIA hold stakes in or contracts with these firms; semiconductor, power, and data-center names monetize the buildout regardless of which lab wins; and established space ETFs (UFO, ROKT, ARKX) offer sector exposure, while leveraged and income ETFs tied specifically to SPCX are already being filed — the latter are best avoided.

Key risks to disclose: unproven public-market valuations against limited audited history; concentrated founder control (Musk holds roughly 85% of voting power); scheduled unlock supply; regulatory exposure (defense concentration, AI policy); competitive margin compression among the labs themselves (Codex and Claude Code are substitutable); and the structural risk that fast-tracked index inclusion transfers early-price-discovery risk to passive holders. A shiny narrative easily blinds investors to these and other landmines we cannot see yet.

Five client discussion questions

If you already hold QQQ, you’ll soon own SpaceX automatically — does adding individual shares double a bet you didn’t know you had?

Are you comfortable buying at a valuation set when only ~7% of listed shares trade freely, knowing scheduled unlocks expand that supply more than tenfold within six months?

What would have to be true in 2031 for a $1.75T (or $1T) entry price to compound at an acceptable rate?

Would you rather own the labs, or the companies selling them compute, power, and chips?

If the answer is “I just don’t want to miss it,” what dollar amount can you lose 50% of without changing your plan?

All valuations, timelines, and pre-listing financial figures are reported estimates from media and company announcements unless drawn from public SEC filings, and are subject to change. Nothing herein is a recommendation to buy or sell any security.

This material is provided for informational and educational purposes only and should not be construed as investment advice, a recommendation to buy or sell any security, or a recommendation to adopt any specific investment strategy.

References to specific companies, sectors, valuation metrics, or historical market periods are included solely for illustrative and discussion purposes. Certain private company valuation, revenue, financing, and market data referenced herein are based on publicly available reports, third party sources, and Modelist Inc. estimates, and have not been independently verified. Forward looking statements, estimates, and historical comparisons are inherently uncertain and may not reflect actual future results. All investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Modelist Inc. is a registered investment adviser. Registration does not imply a certain level of skill or training. Additional information about Modelist, including its Form ADV Part 2A, is available upon request or at www.adviserinfo.sec.gov.